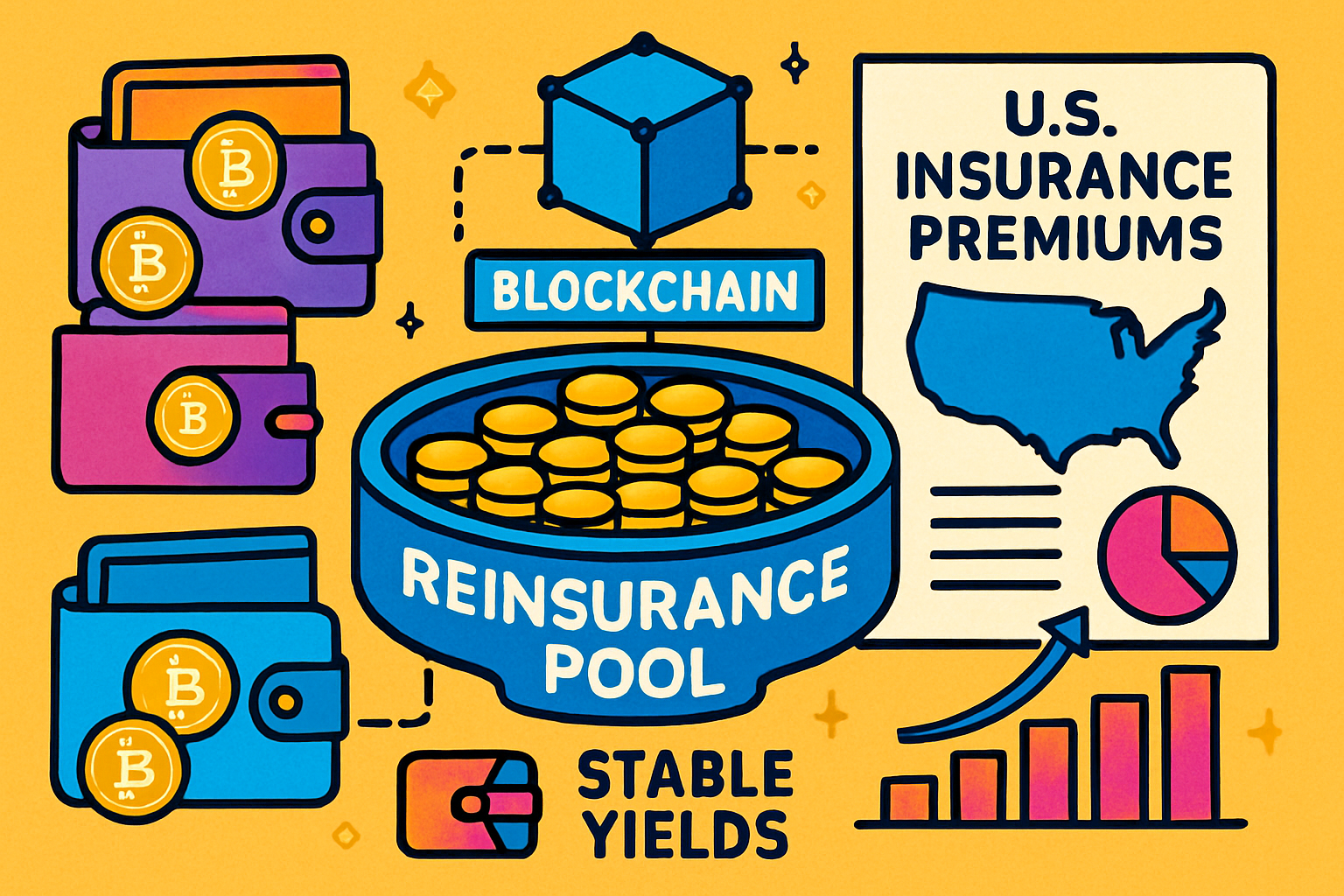

Picture this: while the crypto market swings wildly, you're earning steady yields from the trillion-dollar world of US insurance premiums. That's the promise of on-chain reinsurance pools in 2025, and as a swing trader who's seen every chart pattern under the sun, I can tell you this trend is reshaping how we think about DeFi yields. These pools let you park your stablecoins in fully collateralized risk pools backed by real-world insurance, delivering stablecoin reinsurance yields that beat traditional savings accounts without the drama of memecoins or leveraged trades.

We've hit a tipping point. Retail investors are finally tapping into reinsurance markets that were once locked behind institutional gates. Protocols are tokenizing these opportunities, turning opaque insurance contracts into transparent, on-chain assets. No more waiting for quarterly reports; you see premiums flowing in real-time, claims processing automatically, and your share of the yield accruing steadily.

2025 Performance: Outpacing Traditional Reinsurers

Let's dive into the numbers that make this exciting. In 2025, protocols like Re have crushed it with a stellar 92% combined ratio and $168.8 million in written premiums. That's not just survival in a competitive field; it's outperformance. Traditional reinsurers envy that efficiency, especially as global reinsurance capital swells to $735 billion. For context, the US property and casualty sector holds a stable 10% ROE projection through 2026, providing the bedrock for these US insurance premiums DeFi plays.

Re's growth isn't isolated. OnRe connects on-chain capital to consistent reinsurance returns, backed by regulated businesses. Their protocol token ties directly to revenue streams, while expansions on Avalanche open uncorrelated yields from low-volatility programs. Even newcomers like Falcon Finance launched with $10 million in stablecoins, proving the model's scalability.

Blockchain's Game-Changing Advantages for Reinsurance

What sets tokenized reinsurance 2025 apart? It's the blockchain magic. Smart contracts automate claims, slashing delays from weeks to minutes. Imagine a hurricane hits; predefined parameters trigger payouts instantly, no brokers haggling. Administrative costs plummet thanks to a shared ledger, where everyone audits reserves and premiums in real-time.

Transparency builds trust. As investors, we hate black boxes. Here, you track every dollar of premium income. Programmable capital means directing funds to specific pools, like auto or homeowners insurance, without middlemen skimming fees. This realigns incentives: yields come from actual underwriting profits, not leveraged bets. Check out how these pools generate yield from premiums for a deeper look.

Spotlight on Leading Protocols Driving Stable Yields

Re Protocol leads the pack on Avalanche and Ethereum, offering tokens backed by US underwriting. Their Re protocol reinsurance APY draws crowds with fully collateralized, low-vol structures. Deposit stablecoins, earn from premiums minus claims, and watch uncorrelated returns compound.

OnRe, evolved from Nayms, bridges DeFi to global reinsurance. Diversified pools expose you to premium income plus collateral yields, all regulated for peace of mind. Etherisc shines in parametric niches, auto-paying for flight delays or crop issues via oracles. These aren't hypotheticals; Re's $168.8 million TVL shows capital flowing freely, like any DeFi asset.

Investors love the stability. While crypto yields spike and crash, reinsurance pools hum along at predictable rates, fueled by America's massive P and C market. Backers like RockawayX see OnRe as DeFi's maturity milestone. Opolis even tokenizes healthcare bonds with restaking for extra juice.

From my trading desk, where I've chased breakouts in everything from BTC to blue-chips, this feels like discovering a hidden chart pattern with legs. On-chain reinsurance pools aren't flashy, but they deliver what every savvy investor craves: real-world yields that don't evaporate in a bear market. Picture stablecoins working overtime on US auto and homeowners premiums, churning out stablecoin reinsurance yields backed by regulated underwriting. No vaporware here, just premiums turning into compounding returns.

Let's get practical. These pools target frequency risks, like everyday fender-benders or minor leaks, steering clear of catastrophe exposure. That means 8-15% stable yields without the heart-stopping volatility of hurricanes or earthquakes. Re Protocol's setup on Avalanche shines here, with tokens fully collateralized against low-vol insurance programs. Their expansion unlocks institutional-grade capacity, while $168.8 million TVL proves liquidity matches the hype. As a trader, I appreciate how this mirrors a tight Bollinger Band squeeze: low risk, steady expansion.

OnRe takes it further by linking DeFi liquidity to diversified reinsurance baskets. Deposit USDC, tap into premium flows from America's P and C giants, and layer on collateral yields. It's regulated, so no rug-pull worries, and backers like RockawayX call it DeFi's efficiency leap. Etherisc adds parametric flair, paying out for verifiable events via oracles, perfect for niche plays like travel disruptions. Together, they're democratizing a $735 billion capital pool that traditional players hoard.

Why Yields Beat Crypto Volatility Every Time

In a world of 100x pumps and 90% dumps, US insurance premiums DeFi offers sanity. Traditional reinsurers hit 10% ROE; on-chain versions amp it up through cost cuts. Blockchain zaps admin fees by 30-50%, funnels more to yield. Smart contracts handle claims in blocks, not boardrooms, boosting that 92% combined ratio Re flaunted. Investors earn from investment income on reserves too, creating dual streams uncorrelated to crypto winters.

I've backtested this mentally against my swing trades: reinsurance APYs hover predictably, while alts swing 20% daily. Tokenized reinsurance 2025 isn't about moonshots; it's portfolio ballast. Dive into how these yields stack from auto and homeowners premiums, and you'll see 6-23% ranges tailored to risk appetite. Frequency pools lock 8-15%, severity ones push higher with collars.

Risks? Sure, underwriting glitches or oracle fails, but full collateralization caps downside. Protocols like Re stress-test rigorously, and transparency lets you exit fast. Compare to CeFi collapses: here, your capital backs tangible policies, audited on-chain. Global capital at $735 billion signals room to grow, with retail inflows just starting.

Opolis innovates on healthcare, blending restaking for boosted bonds that cut costs and return profits. Falcon's $10 million launch shows even DeFi natives pivot to insurance yield. As chains like Avalanche scale, capital flows freer, mimicking DEX liquidity for reinsurance.

Smart money positions now. These pools aren't fringe; they're the bridge from crypto speculation to institutional-grade returns. Every chart tells a story, and this one's plotting steady uptrends amid market noise. Grab stablecoins, pick your protocol, and let US premiums fuel your next trade. The reinsurance revolution is live, yielding stability in a chaotic crypto era.

No comments yet. Be the first to share your thoughts!