DeFi capital faces growing exposure

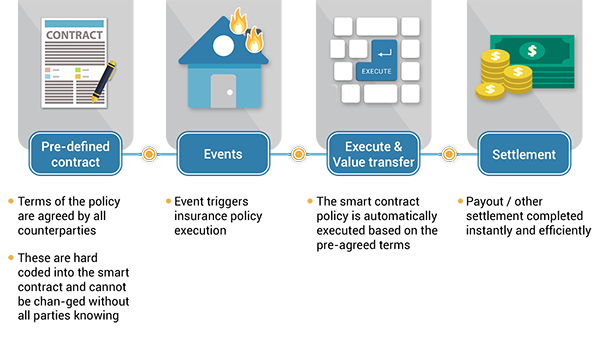

Smart contract risk is no longer a niche concern; it is the central vulnerability in the 2026 market cycle. As decentralized finance protocols manage larger treasuries, the potential for catastrophic loss from code exploits or oracle failures has scaled proportionally. Traditional insurance models struggle to underwrite this dynamic risk, creating an urgent need for institutional-grade protection mechanisms that can settle claims instantly and transparently.

The scale of capital at risk is evident in the broader market movements. Traders and protocols are closely monitoring total value locked (TVL) and volatility metrics to gauge systemic health.

This exposure has pushed the industry toward specialized reinsurance solutions. Platforms like Re are already authorizing significant capacity, such as the US$134 million in reinsurance capacity authorized for 2026 renewals, to backstop these digital assets. Without such infrastructure, the fragility of unsecured DeFi positions remains a critical barrier to broader institutional adoption.

Re platform deploys $134 million for renewals

The scale of capital deployment in decentralized reinsurance has shifted from experimental pilots to institutional-grade commitments. Leading blockchain reinsurer Re has authorized $134 million in reinsurance capacity across multiple programs ahead of the January 2026 renewals. This move signals a maturation in how crypto-native protocols manage tail risk, moving beyond simple liquidity pools to structured, multi-program capital deployment.

Unlike traditional reinsurance, which relies on complex balance sheet structures and long settlement cycles, Re’s platform automates the binding and settlement of these large-scale policies through smart contracts. The $134 million figure represents not just capital, but verified on-chain liquidity that is immediately available to cover potential claims. This transparency reduces counterparty risk, a persistent issue in traditional reinsurance markets where solvency can be opaque.

The deployment covers a diversified range of crypto-specific risks, including smart contract vulnerabilities, custodial failures, and oracle manipulations. By aggregating this capital into a single, auditable platform, Re allows insurers to access reinsurance coverage without the friction of traditional broker intermediaries. This efficiency is critical as the industry faces a hard market, with traditional reinsurers pulling back from high-risk crypto exposures.

The decision to lock in this capacity ahead of the renewal cycle reflects a proactive approach to risk management. Insurers using the platform are securing coverage at a time when traditional capacity is tightening and pricing is rising. This shift underscores the growing reliance on DeFi infrastructure to provide financial stability in a volatile asset class.

Traditional reinsurers enter the blockchain space

For decades, the reinsurance industry operated in a silo of paper contracts and quarterly audits. That era is ending as legacy giants like Munich Re begin to underwrite digital asset risk directly. This shift marks the first time traditional capital is flowing into DeFi risk pools, bridging the gap between regulated finance and decentralized protocols.

Munich Re’s entry into digital asset protection signals institutional validation for crypto insurance. Their tailored products target professional custodians and institutional holders, offering coverage for theft, loss, and operational failures. By bringing actuarial rigor to blockchain risks, they are creating a safety net that DeFi alone has struggled to build.

The appeal for traditional reinsurers is clear: blockchain offers unprecedented transparency. Every transaction on the ledger is immutable and visible, reducing the information asymmetry that has long plagued risk assessment. This data-rich environment allows for more precise pricing and faster claims processing compared to legacy methods.

However, the integration is not without friction. Traditional underwriters must adapt to the 24/7 nature of crypto markets and the unique code vulnerabilities of smart contracts. The result is a hybrid model where legacy capital meets decentralized innovation, creating a more robust infrastructure for digital asset protection.

| Feature | Traditional Reinsurance | DeFi Insurance |

|---|---|---|

| Transparency | Limited, periodic reports | Real-time on-chain data |

| Speed | Weeks to months | Automated, near-instant |

| Coverage Scope | Broad, physical assets | Smart contract, custody risk |

Smart contract audits drive demand

The foundation of crypto reinsurance is not capital, but code. Before a DeFi protocol can secure coverage, it must prove its smart contracts are free from critical vulnerabilities. This requirement has turned rigorous security audits into a non-negotiable prerequisite for risk mitigation. Without this technical proof, traditional reinsurance models simply cannot function in the decentralized space.

Audit firms now serve as the gatekeepers of insurability. They perform deep-dive analyses of protocol logic, identifying edge cases that could lead to exploits or fund drains. These reports provide the actuarial data needed to price risk accurately. If an audit reveals high-severity issues, coverage is typically denied or priced prohibitively high, forcing protocols to patch vulnerabilities before seeking protection.

This dynamic creates a direct link between security hygiene and insurance affordability. Protocols that invest in comprehensive audits and bug bounty programs signal lower risk to reinsurers. As the industry matures, the standard for these technical prerequisites is rising, making thorough security reviews the primary driver of demand for specialized crypto insurance products.

Global Reinsurance Outlook 2026

The traditional reinsurance market is undergoing a significant recalibration in 2026. According to Fitch Ratings, global reinsurers are expected to see profitability decline this year, although earnings will remain at sound levels overall [[src-serp-8]]. This shift is largely driven by contract renewals in January, which confirmed further reductions in risk-adjusted prices across most lines. As capacity tightens and pricing softens, the broader industry is looking for new avenues of growth and capital deployment.

This macroeconomic pressure creates a distinct opening for niche digital asset lines. While traditional perils face margin compression, the volatility and complexity of crypto assets have historically commanded higher premiums. For reinsurers seeking to offset declines in legacy lines, crypto reinsurance offers a specialized pocket of demand where technical expertise can still command a premium. The convergence of traditional capital constraints and emerging digital risks is reshaping how global players view hedging strategies.

The broader landscape is also seeing increased interest in alternative capital sources. Industry events, such as the upcoming Re/insurance Outlook Europe conference in Zurich, are focusing heavily on resilience and emerging risks [[src-serp-4]]. As traditional models adapt to a lower-margin environment, the integration of decentralized finance (DeFi) protocols into the reinsurance stack represents a structural shift rather than a temporary trend. Crypto reinsurance is no longer just an experiment; it is becoming a necessary component of a diversified risk portfolio in a tightening market.

Frequently asked questions about crypto insurance

Will bitcoin ever be insured?

Yes, but coverage is currently limited to specific institutional players rather than individual retail holders. Traditional government protections like the FDIC or SIPC do not extend to digital assets, meaning most crypto holdings remain uninsured against exchange failures or hacks. However, specialized providers like Munich Re are developing tailored products for professional custodians and institutional holders, creating a parallel insurance market for large-scale digital asset protection.

What is the outlook for reinsurance in 2026?

The reinsurance market is tightening as global reinsurers face declining profitability. According to Fitch Ratings, contract renewals in January confirmed further reductions in risk-adjusted prices across most lines. While earnings are expected to remain at sound levels, the overall outlook for global reinsurers is deteriorating, which may lead to stricter underwriting standards and higher premiums for crypto-specific risk transfers.

How does DeFi insurance differ from traditional policies?

DeFi insurance relies on smart contracts and pooled capital rather than traditional actuarial models. Protocols like Nexus Mutual or InsurAce allow users to buy coverage using tokens, with claims paid out from community-managed funds. This model offers transparency and instant payouts for verified exploits but lacks the regulatory oversight and capital reserves of traditional insurers, making it a high-risk, high-reward alternative for hedging protocol-specific vulnerabilities.

No comments yet. Be the first to share your thoughts!