Capital Deployment in 2026 Renewals

The January 2026 renewal cycle marked a distinct shift in capital flow toward decentralized reinsurance infrastructure, signaling a maturation of tokenized capacity within traditional treaty placements. Leading this movement, blockchain-focused reinsurer Re authorized $134 million in reinsurance capacity across multiple programs. This deployment underscores a growing willingness among institutional participants to allocate significant capital to digital asset risk transfer mechanisms, moving beyond pilot projects into substantial, measurable market participation.

This influx of capital arrives as the broader reinsurance sector navigates a complex pricing environment. According to S&P Global Ratings, reinsurers entered 2026 from a position of capital strength, with earnings supported by robust investment income. However, underwriting performance faces increased pressure as reinsurance pricing moderates. The contrast between traditional rate softening and the steady deployment of blockchain-based capital highlights a divergence in risk appetite and capacity sourcing strategies.

Market data from A.M. Best indicates that property reinsurance rates fell between 10% and 20% at the January 1, 2026, renewal, particularly on accounts with no prior loss history. In this context, the $134 million commitment by Re represents not just volume, but a strategic positioning in a market where traditional capacity is becoming more price-sensitive. The integration of tokenized capacity offers a potential hedge against the volatility of traditional treaty pricing, providing a liquid and transparent alternative for risk transfer.

To contextualize the capital flows within the broader digital asset market, the following chart illustrates the performance of a relevant crypto market index, reflecting the macroeconomic environment in which these insurance-linked instruments operate.

The deployment of this capital suggests that digital asset insurers are increasingly viewed as viable counterparties in the traditional reinsurance market. As regulatory clarity improves and technical infrastructure matures, the alignment between blockchain efficiency and traditional risk pooling mechanisms is likely to deepen, potentially reshaping how capacity is sourced and priced in subsequent renewal cycles.

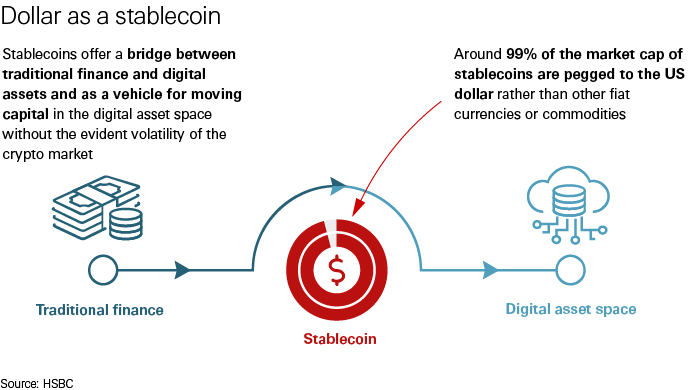

Regulatory compliance and stablecoin premiums

The regulatory landscape for crypto risk transfer is shifting from speculative experimentation to structured compliance. As the 2026 renewal period progresses, the integration of stablecoins into traditional reinsurance workflows has moved beyond pilot programs to become a recognized mechanism for premium settlement. This transition is driven by the need for finality and speed in cross-border transactions, aligning digital asset payments with established insurance accounting standards.

A significant milestone was reached in March 2026 when Aon executed what is reported as the first known stablecoin insurance premium payment among major brokers. This transaction signals a tangible shift in regulatory acceptance, demonstrating that major intermediaries can navigate anti-money laundering (AML) and know-your-customer (KYC) requirements when using regulated stablecoins. Such adoptions provide a blueprint for how legacy insurance infrastructure can accommodate crypto-native payment rails without compromising compliance integrity.

Parallel to payment innovations, the creation of regulated reinsurance vehicles is expanding capacity for crypto-specific risks. Relm Insurance announced the launch of Relm II, a dedicated reinsurance entity designed to provide regulated capacity for companies operating in the digital asset space. By establishing a legally distinct vehicle with clear capitalization requirements, Relm II addresses the regulatory uncertainty that has historically hindered large-scale crypto insurance placements. This structure allows insurers to offload risk to reinsurers who understand the unique volatility and technological risks inherent in blockchain assets.

The broader reinsurance market in 2026 is characterized by ample capacity but moderating prices. While property reinsurance rates fell between 10% and 20% during the January 1, 2026, renewal period, the crypto sector remains distinct due to its specialized risk profile. The combination of regulated vehicles like Relm II and compliant payment methods like stablecoin premiums creates a more stable foundation for underwriting crypto assets. This structural clarity is essential for attracting institutional capital and ensuring long-term solvency in a high-stakes market.

DeFi solvency protocols and on-chain transparency

Traditional reinsurance operates behind closed doors, relying on quarterly audits and opaque bilateral contracts to verify capital adequacy. For DeFi protocols, this latency creates significant counterparty risk and opacity. On-chain reinsurance markets address this structural deficiency by anchoring capital verification to real-time, immutable ledger data. This shift transforms solvency from a retrospective accounting exercise into a continuous, programmable state.

The January 1, 2026, renewal period highlighted the urgency of this transition. As A.M. Best reported, property reinsurance rates fell between 10% and 20% during this cycle, with the sharpest declines observed on accounts with no prior loss history. This moderation in pricing, coupled with ample capacity, has intensified competition among traditional reinsurers. In this environment, DeFi protocols require immediate visibility into the liquidity backing their risk layers to maintain trust and regulatory compliance.

On-chain protocols replace manual verification with smart contract-enforced transparency. Capital allocation is visible to all participants, eliminating the information asymmetry that characterizes traditional markets. This clarity allows DeFi protocols to price risk more accurately and settle claims instantly, reducing the operational drag inherent in legacy systems.

The following comparison illustrates the operational divergence between legacy and on-chain structures.

| Feature | Traditional Reinsurance | On-Chain Reinsurance |

|---|---|---|

| Capital Verification | Quarterly audits, opaque bilateral contracts | Real-time, immutable ledger data |

| Settlement Speed | Days to weeks, manual processing | Instant, smart contract-enforced |

| Pricing Transparency | Limited, based on proprietary models | Public, algorithmic, and auditable |

This transparency is critical for institutional adoption. As S&P Global noted in its 2026 global reinsurance sector view, reinsurers are entering the year with capital strength, but underwriting performance faces pressure. For DeFi, on-chain solvency protocols provide the necessary audit trail to demonstrate resilience against these market shifts, ensuring that capital is both available and verifiable when claims arise.

General property rates soften while crypto reinsurance holds firm

The broader reinsurance market is navigating a distinct bifurcation in 2026. General property reinsurance rates have softened, with the January 1 renewal period seeing declines of 10% to 20% on accounts with no prior loss history, according to A.M. Best. This moderation reflects ample capacity and intensifying competition across traditional lines, a trend noted by S&P Global Ratings as a primary driver of underwriting pressure this year.

Crypto reinsurance remains insulated from these generalist trends. Unlike standard property lines, specialized crypto reinsurers operate with rigorous, asset-specific risk models that account for unique blockchain vulnerabilities, such as smart contract exploits and custody failures. These models do not rely on the same historical loss data that drives traditional property pricing, creating a barrier to entry that prevents generalist insurers from flooding the space with cheap capital.

The financial resilience of specialized reinsurers provides a stable foundation for this niche. Genesis Global Re notes that reinsurers are entering 2026 with stronger balance sheets and better capital buffers. This financial strength allows them to make deliberate, long-term decisions about capital deployment rather than chasing short-term market share. This stability is critical for crypto projects, which require partners capable of absorbing volatile, high-severity losses without compromising solvency.

The divergence between softening general rates and stable crypto reinsurance pricing highlights the value of specialized underwriting. For crypto firms, the cost of capital is less about market-wide rate fluctuations and more about the precision of risk assessment. Specialized reinsurers offer this precision, ensuring that pricing reflects the true underlying risk of digital asset exposure rather than general market sentiment.

No comments yet. Be the first to share your thoughts!